A Practical Restaurant Strategy Series (EP 1–2)

EP 1: Designing Cost, Not Just Cutting It

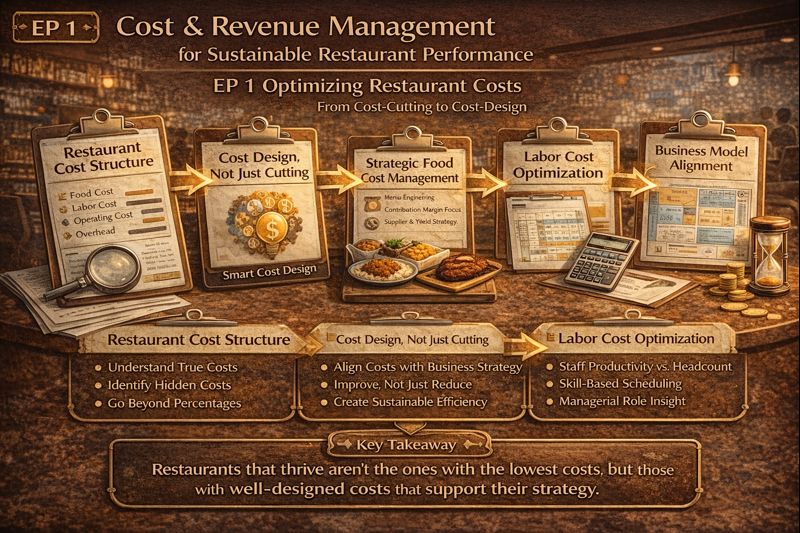

Understanding Restaurant Cost Structure as a Strategic System

By Charles Tan

Introduction

Many restaurants fail not because they lack customers, but because they lack cost clarity. Operators often track percentages—food cost, labor cost, overhead—but fail to understand how these costs are created, connected, and controlled.

Sustainable restaurants do not simply reduce costs. They design costs deliberately, aligning them with their concept, customer expectations, and operating model.

- The True Cost Structure of a Restaurant

A restaurant’s cost base typically consists of:

- Food & Beverage Cost – ingredients, waste, yield, purchasing strategy

- Labor Cost – staffing levels, productivity, skill mix, scheduling

- Operating Costs – utilities, supplies, maintenance, technology

- Overhead & Fixed Costs – rent, administration, depreciation, financing

The most common mistake is knowing the percentages but not understanding what drives them.

- From Cost Cutting to Cost Design

Reactive cost cutting often damages quality, morale, and brand perception. Cost design, by contrast, asks a different question:

What level of cost is appropriate to deliver the value we promise?

Cost design aligns:

- Menu complexity with kitchen capability

- Service style with labor structure

- Supplier choices with volume and positioning

- Strategic Food Cost Management

Effective food cost control is not about cheaper ingredients; it is about:

- Menu engineering based on contribution margin

- Portion control without reducing perceived value

- Yield management across preparation and production

- Supplier partnerships, not transactional buying

- Labor Cost as a Productivity System

Labor is the most emotionally managed cost—and the most dangerous when unmanaged.

Key principles:

- Productivity over headcount reduction

- Skill-based scheduling

- Clear role design and workflow discipline

- Manager accountability at shift level

- Linking Cost Structure to the Business Model Canvas

Within the Business Model Canvas, Cost Structure must align with:

- Value Proposition

- Customer Segments

- Key Activities

When costs contradict the value offered, profitability becomes structurally impossible.